New banking with blockchain – are we there yet?

New Banking // Disruption, revolution, and tech giants as the new bankers – these buzzwords keep coming up in the conversation about new banking and blockchain in the world of finance. What has happened to this revolution? Is the dream still alive, or is it a bubble that’s about to burst? In this article, we share some insights and updates from the fintech scene.

Blockchain technology has been around for 14 years now, and there’s been no holding back on the superlatives during this time. The enormous potential this technology has to offer in various sectors is reiterated again and again, especially when it comes to potential disruption in the banking industry. It’s a sector that loves to make big announcements about the bright future ahead and draw attention to itself even when projects are still in the early stages of development. The other side of the finance industry is made up of big banks that warn against cryptocurrencies, highlight how much energy the technology consumes, and paint a picture of users working with dirty money. Or, to exaggerate, we could say this is an arena in which innovative gold diggers come up against traditional, risk averse bankers.

A roller-coaster ride

The development of the fintech sector with its capabilities, experience, and latest standard of technology is progressing rapidly thanks to its tireless pioneering spirit. Neobanks have succeeded in positioning themselves in the market, offer a better customer experience, and demonstrate that banking can be done in a different way. At the same time, Swiss fintech companies in particular are struggling with growth. Fintechs are alternately heaped with praise or written off, and this emotional roller coaster can also be felt in the industry when it comes to digital assets. A wave of excitement about initial coin offerings (ICOs) was followed by a crypto winter, with this being closely succeeded in turn by a spring filled with security token offerings (STOs), decentralized finance (DeFi), and NFTs. At present, there is talk of another crypto winter. The media’s perspective on the fintech scene is often superficial and oversimplified. As a result, the exchange rates are seen as representative of the state of health of an entire sector. But little attention is given to the rocky road this revolutionary technology has traveled.

Digitalization and decentralization play a pivotal role in an enthusiastic, free-thinking, and globally active community. Companies, politicians, and regulators quickly realized that this development, together with the megatrends of the Internet and smartphones, would push past boundaries and pave the way for a multitude of changes. As is always the case with developments offering great potential for change, concerns were raised, bans were put in place in some countries, and the risks presented by a young technology were emphasized. This was justified to some extent because cunning “entrepreneurs” and individuals with criminal intent flagrantly exploited the edge they had with regard to knowledge and technology. Huge sums of money were lost in attractive-looking business models by companies working in legal gray areas, and honeypots were hacked. A suspect image was born, and the campaign against the fintech scene was launched.

The potential

Every crisis generates opportunities – and this maxim applies to the fintech sector, too. In every crisis, weak business models were eliminated first and foremost, with new companies being founded based on what had been learned. As part of this, a certain degree of standardization is also developing around technologies over time. One example is the solid solutions that have been developed in the area of digital asset storage in recent years. Lawmakers, especially in Switzerland and the EU, have put positive framework conditions in place. This is creating legal security for investors and those making use of new, innovative business ideas. Trading digital stocks, bonds, and shares in funds via a regulated trading infrastructure represents another key step in the development of the fintech scene. The awarding of the first licenses in Switzerland in the coming months is a highly anticipated development. It creates the impression that the legal framework and the financial market infrastructure in Switzerland are ready for the innovative world of tomorrow’s finance. This impression isn’t inaccurate. But many challenges still lie ahead.

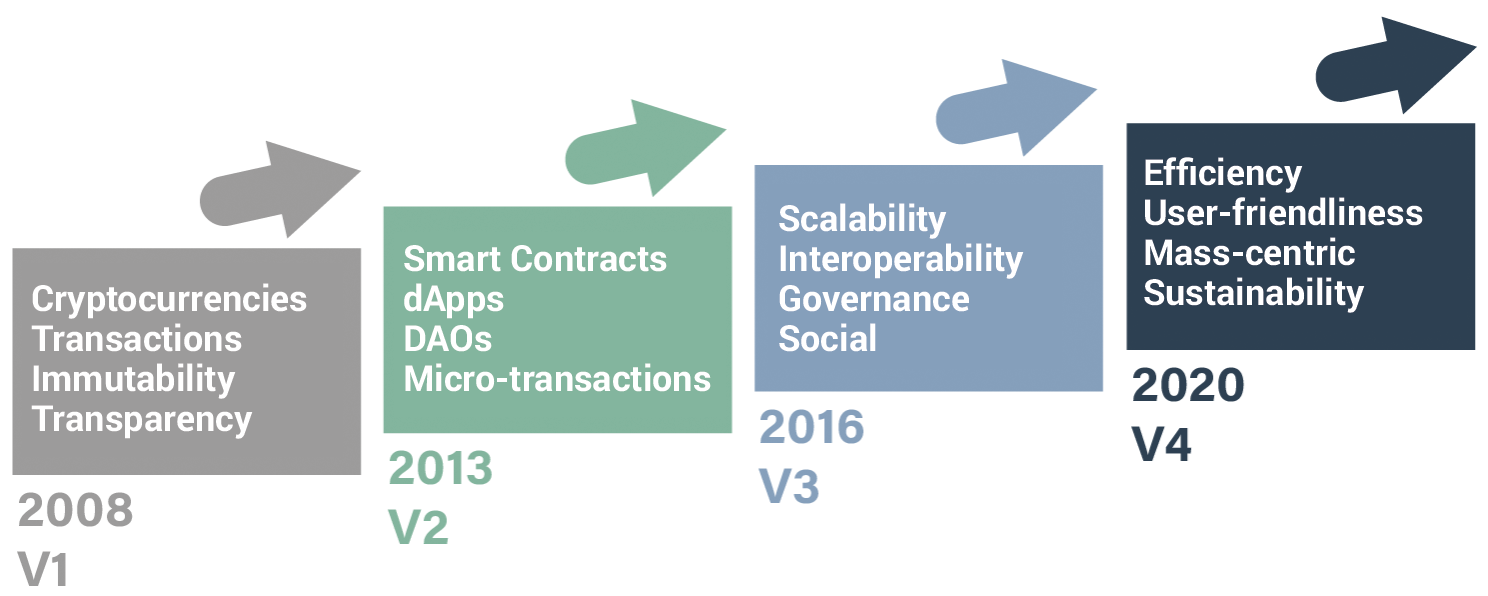

From challenger to mainstream suitability: the evolution of the blockchain ecosystem

From challenger to mainstream suitability: the evolution of the blockchain ecosystem

The challenges

A new business model always has to accommodate all technical, legal, and economic aspects in order to be successful on the market. Moreover, the disruptive potential offered by such business models must not take effect abruptly, as this often requires changes in the entire financial market system. The sector is developing by leaps and bounds, continually presenting new use cases as it does so. Regulation is lagging behind, as it must. Key questions, such as the (legal) approach to decentralized structures (smart contracts or decentralized stock exchanges), for instance, still need to be resolved. New ways of thinking are needed in order to allow for valuable innovations while simultaneously upholding the goals that regulation aims to achieve, such as protecting investors or ensuring system stability. In addition to these unresolved areas around business and legal matters, there is also the biggest challenge of all: willingness to accept change. Not all of the players in the financial market have the same capacity for innovation and dealing with transformation. Even today, many are resisting this process rather than getting involved in shaping it themselves. Major changes are stymied by the fact that large organizations tend to be less nimble as well as the psychological aspect that the human brain perceives transformation as conflict.

The approach

A new way of doing banking needs to be created for young generations. Today’s financial institutions have to make a choice: They can assume an open attitude and take a close-up look at the areas of application offered by new technologies, dare to take the first steps, and benefit from increased efficiency, service innovations, and customer growth in the coming years – or face the risk of being shut out as a player on the market in the future. This process gets exciting when, as is the case now, established participants aren’t the only ones working to transform the financial system – rather, players from outside the old system are driving the change as well. This results in a new way of looking at the existing services and thus the opportunity to build a more advantageous system for the ecosystem as a whole.

AI-and-Open-Source, Special

“We need more courage in AI projects”

AI made in Lucerne // While tech giants are pumping billions into AI infrastructure, the Applied AI Center of the Lucerne School of Computer Science and Information Technology at Lucerne University of Applied Sciences and Arts is taking a different approach: Donnacha Daly, one of the Center’s co-founders, explains why open source could save our digital independence and why, paradoxically, the future of AI lies in smaller models.

Donnacha Daly - Mar 25, 2026

Special, Digital-Trust

Trust is the key to success

Andreas Tölke - Jun 26, 2024